Nvidia revenue multiple is one of the most debated valuation metrics in the market, and if you are trying to judge whether NVDA is expensive, fairly priced, or a bargain in disguise, this is the number you need to understand properly. The problem is that a raw price-to-sales figure means nothing without context. This review explains what the revenue multiple actually measures, how to interpret it against growth and peers, and how recent catalysts factor in, so you can form a grounded valuation view instead of reacting to a scary-looking ratio.

What the Nvidia Revenue Multiple Really Measures

Before deciding whether Nvidia’s multiple is too high, you need to know exactly what it is and why analysts use it. This section defines the price-to-sales ratio, explains why the revenue multiple is especially relevant for a high-growth company like Nvidia, and shows how growth rates change what a “fair” multiple looks like.

Understanding Price-to-Sales Basics

The revenue multiple, or price-to-sales ratio, divides a company’s market capitalization by its annual revenue. It tells you how many dollars investors are paying for each dollar of the company’s sales.

Unlike the price-to-earnings ratio, the revenue multiple works even when earnings are volatile or reinvested heavily, which is why it is a common tool for growth companies. It focuses on the top line rather than the bottom line.

For a company like Nvidia, this makes the metric useful for comparing valuation across time and against peers, as long as you remember it ignores profitability and margins entirely.

A simple way to internalize it: a price-to-sales ratio of ten means investors are paying ten dollars for every dollar of annual revenue the company generates. Whether that is reasonable depends entirely on how fast and how profitably that revenue is expected to grow.

Why It Matters for High-Growth Nvidia

Nvidia has historically traded at a high revenue multiple, and on the surface that looks alarming. But a multiple must always be read against growth: a company doubling its revenue justifies a far higher multiple than one growing slowly.

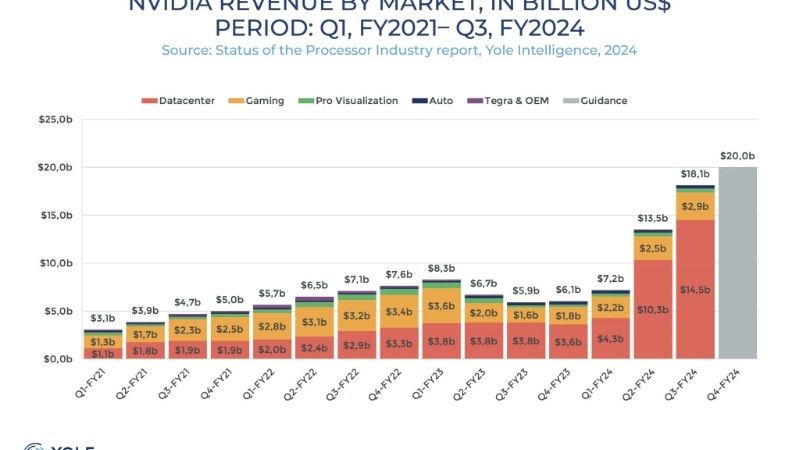

Because Nvidia’s data center revenue has grown explosively, investors have been willing to pay a premium multiple, betting that today’s sales are a fraction of tomorrow’s. The multiple prices in future growth, not just current sales.

The practical point is that a high revenue multiple is not automatically a warning sign. It is a statement about expectations, and whether it is justified depends entirely on whether that growth materializes.

How Growth Rates Reshape a Fair Multiple

The single most important context for any revenue multiple is the growth rate behind it. A useful mental model is that the faster and more durable the revenue growth, the higher the multiple the market will rationally assign.

If Nvidia’s growth stays strong, a multiple that looks stretched today can normalize quickly as sales catch up. If growth slows, the same multiple suddenly looks expensive, and the stock can de-rate sharply.

This is why sophisticated investors pair the multiple with growth expectations rather than judging it in isolation. The number alone is meaningless without the growth story attached.

Historically, Nvidia’s own multiple has swung widely as the market’s growth expectations shifted. Studying how the ratio expanded and contracted over past cycles is a useful reality check — it shows that today’s figure is one point on a long, volatile line, not a fixed truth.

Putting the Multiple in Context

A revenue multiple only becomes useful when compared — to peers, to history, and to the catalysts that could change the trajectory. This section benchmarks Nvidia against other chipmakers, examines how the H200-to-China opening affects the revenue outlook, and weighs the honest pros and cons of relying on this metric.

Comparing Nvidia to Semiconductor Peers

Nvidia typically trades at a higher revenue multiple than most semiconductor peers, and the reason is its growth and margins. A commodity chipmaker growing slowly deserves a low multiple; a company dominating the AI accelerator market with high margins commands more.

When comparing, it is essential to compare like with like: match growth rates and profitability, not just the raw multiple. A peer with a lower multiple may simply be growing far slower.

The takeaway is that Nvidia’s premium over peers is not inherently irrational. It reflects a genuinely different growth and margin profile, though whether the premium is too large is the real debate.

It is also worth comparing Nvidia against high-growth software companies, not just chipmakers, since the market increasingly values it partly on its software-driven moat. That cross-sector view sometimes makes the multiple look more reasonable than a pure semiconductor comparison suggests.

The trap to avoid is anchoring on a peer’s lower multiple as proof that Nvidia is overpriced. If that peer is growing at a fraction of Nvidia’s rate, the lower multiple is exactly what theory predicts — it is not evidence of a bargain.

How the H200-to-China Deal Affects the Outlook

A concrete catalyst now factors into the revenue picture: the United States has cleared Nvidia to sell its H200 chip — one of its most powerful AI processors — to China, reopening access to a large market that restrictions had limited.

For the revenue multiple, this matters because incremental sales into China could lift the revenue denominator, which would mechanically lower the multiple if the market cap stays constant. More sales for the same price means a cheaper multiple.

The forward-looking caveat is that this depends on how much revenue actually materializes and how durable the policy is. It is a potential tailwind to the top line, but one tied to a regulatory backdrop that can shift.

For a valuation analyst, the cleanest way to handle a catalyst like this is scenario modeling: estimate the multiple under a conservative revenue case and an optimistic one. The gap between those scenarios shows how much of the current price depends on the China opening actually delivering.

Pros and Cons of Using the Revenue Multiple

Relying on the revenue multiple has clear strengths and clear limits. The pros: it works even when earnings are noisy, it is simple to calculate and compare, it is useful for high-growth companies, and it captures the market’s growth expectations in a single number.

The cons: it completely ignores profitability and margins, it can look misleadingly high for fast growers, it says nothing about debt or cash flow, and it is easy to misuse by comparing companies with very different growth profiles.

The pattern is clear. The revenue multiple is a useful starting point but a poor finishing point. It should be one input among several, never the sole basis for a valuation decision.

How to Use the Multiple in Your Own Analysis

Understanding the metric is only valuable if you can apply it, so this section offers a practical framework for using the revenue multiple wisely, the other metrics to pair it with, and a final assessment of what it tells you about NVDA today. None of this is investment advice — consulting a licensed advisor before acting is wise.

Pairing the Multiple With Other Metrics

The revenue multiple should never stand alone. Pair it with the growth rate to see if the multiple is justified, with gross margins to confirm the revenue is high quality, and with the forward price-to-earnings ratio to check profitability expectations.

Looking at the forward multiple — based on next year’s expected revenue rather than trailing sales — often tells a very different, more reasonable story for a fast grower. Trailing numbers understate how quickly the picture can change.

This multi-metric approach protects you from the classic trap of dismissing a stock as overvalued on one scary ratio, or buying it on one cheap-looking one.

Cash flow deserves special attention alongside the multiple. A company converting its revenue into strong free cash flow can support a higher valuation than one that cannot, because that cash funds growth, buybacks, or a cushion in a downturn. Revenue quality, not just revenue quantity, drives a fair multiple.

Watching for a De-Rating Risk

The main danger with a high revenue multiple is de-rating: if growth disappoints, the market lowers the multiple it is willing to pay, and the stock can fall even if revenue still rises. This is the key risk for any premium-multiple stock.

To monitor it, track the revenue growth rate each quarter and watch guidance closely. A deceleration is the early warning that a multiple compression could follow.

The practical discipline is to size your conviction to the growth durability. The more confident you are that growth persists, the more comfortable a high multiple should make you — and vice versa.

It also helps to decide in advance what evidence would change your mind. Setting a mental threshold — for instance, a specific slowdown in data center growth — keeps your reaction disciplined rather than emotional when the next volatile quarter arrives.

Final Assessment of Nvidia’s Valuation

Weighing everything, Nvidia’s revenue multiple is high but not automatically irrational. It reflects strong growth, dominant market position, and high margins, and catalysts like the H200-to-China opening could support the revenue base further.

The honest conclusion is that whether the multiple is justified depends on your view of growth durability and competition. Bulls see a reasonable price for exceptional growth; bears see expectations that leave no room for error.

For your own analysis, use the multiple as one lens among several and keep tracking the fundamentals that drive it. To stay grounded, following each quarter’s revenue and guidance is the smartest ongoing habit before making any decision.

See More:

- 3060 Ti vs 9060 XT

- Nvidia Shield TV Pro

- RTX 5070 vs RX 9060 XT

- RTX 3090 24GB

- Nvidia price prediction

Conclusion

The Nvidia revenue multiple is a powerful but easily misread metric: high on the surface, yet potentially reasonable once you account for the company’s explosive growth, strong margins, and catalysts like the H200-to-China opening. Judged in isolation it looks expensive; judged against growth, peers, and the forward outlook, the picture is far more nuanced. The right approach is to pair the multiple with other metrics, watch for de-rating risk, and match your conviction to growth durability. Keep tracking Nvidia’s quarterly revenue and guidance so your read on the revenue multiple stays current. This article is informational and not financial advice.

Write Your Review

No reviews yet. Be the first to share your experience!