Nvidia revenue growth has been the defining story of the AI era, but if you are an investor or researcher, the headline numbers are only useful once you understand what actually drives them and whether the pace can continue. You want the segments behind the growth, the catalysts, and the honest risks laid out clearly rather than buried in a long video. This review breaks down where Nvidia’s revenue comes from, why it has grown so fast, and the factors that will determine whether the momentum holds.

What Is Actually Driving Nvidia Revenue Growth

Nvidia’s revenue expansion is not evenly spread across its business — it is concentrated in one dominant engine with supporting contributors. This section breaks down the data center segment that powers most of the growth, the role of gaming and other divisions, and the AI demand cycle underpinning the whole story.

The Data Center Segment Dominance

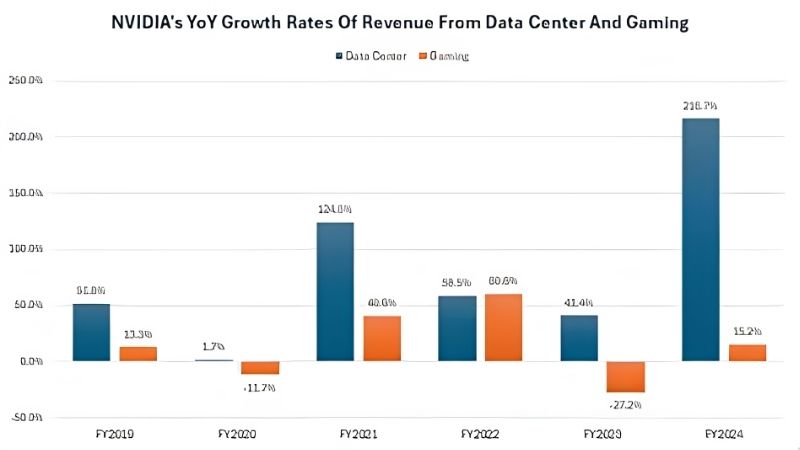

The overwhelming driver of Nvidia revenue growth is its data center segment, which has expanded to represent the large majority of total revenue. Sales of AI accelerators to cloud providers and enterprises building AI infrastructure are the core engine.

This segment has grown at a pace rarely seen in large companies, transforming Nvidia from a graphics specialist into an AI infrastructure giant. The scale of demand for its GPUs is the single biggest reason the top line has surged.

For anyone tracking the company, the practical point is that data center performance essentially is the growth story. Watching this segment tells you almost everything about the near-term trajectory.

This concentration cuts both ways. It has delivered spectacular gains on the way up, but it also means the growth narrative is unusually dependent on a single demand source — a dynamic worth keeping front of mind when interpreting any quarter’s results.

Gaming and Other Segments

While data center dominates, gaming remains a meaningful contributor. Nvidia’s GeForce GPUs continue to sell into a large gaming market, providing a substantial, more stable revenue base alongside the explosive AI growth.

Other segments, including professional visualization and automotive, add smaller contributions. These diversify the revenue mix but are dwarfed by the data center engine in terms of growth impact.

The takeaway is that gaming provides ballast while data center provides the growth. Together they give Nvidia both a steady foundation and an extraordinary growth driver, though the balance has tilted heavily toward AI.

This diversification matters for resilience. If AI demand ever cooled, the gaming and other segments would not replace that growth, but they would cushion the business, giving Nvidia a more stable base than a pure AI pure-play would have.

The AI Demand Cycle

Underpinning everything is the AI demand cycle. The race to build generative AI capability has driven hyperscalers and enterprises to invest enormously in compute, and Nvidia’s GPUs are the default choice for that work.

This cycle has been the rocket fuel behind revenue growth, with multi-year commitments from major customers suggesting the demand is structural rather than a passing spike. As long as AI investment stays strong, the growth engine keeps running.

The forward-looking question is how long this cycle lasts. Its durability is the central variable in any assessment of whether Nvidia’s revenue growth can be sustained.

One indirect factor shaping the cycle is the broader hardware supply chain. Memory pricing, for example, has trended upward and only recently plateaued, and new capacity from suppliers like CXMT and Micron’s planned Idaho fabs is not expected until roughly 2027–2028. Supply constraints across the chain can influence how quickly AI demand converts into shipped revenue.

Catalysts and Risks to Future Growth

Understanding what drives growth is only half the picture; the other half is what could accelerate or derail it. This section examines the H200-to-China catalyst, the competitive and cyclical risks, and the honest pros and cons of Nvidia’s growth outlook.

The H200-to-China Catalyst

A significant recent development is that the United States has cleared Nvidia to sell its H200 chip — one of its most powerful AI processors — to China. This directly affects the revenue growth outlook by reopening access to a large market that export restrictions had constrained.

For revenue growth, incremental sales into China represent potential upside that conservative models may not fully capture. A market of that size returning to the addressable pool is a genuine tailwind for the top line.

How much this contributes depends on demand and competition within that market, where local alternatives also compete. The opening is a positive, but its scale should be watched in actual reported results rather than assumed from the headline alone.

The forward-looking caveat is that this access is tied to policy, which can change. The catalyst is real, but its contribution depends on how much revenue materializes and how durable the regulatory approval proves. For that reason, investors tend to treat it as potential upside rather than baking it fully into their base-case growth expectations until the shipments show up in reported results.

Competition and Cyclical Risks

The biggest threats to sustained growth are competition and cyclicality. Rival chipmakers are pushing their own AI accelerators, and major cloud customers are designing custom silicon to reduce dependence on Nvidia — both of which could slow revenue growth over time.

Semiconductor demand has historically been cyclical, and bears warn that the current AI buildout could eventually normalize into a slower digestion phase. Heavy customer concentration adds risk, since a pullback by a few large buyers would hit results hard.

For an investor, these are the factors to monitor. The growth has been extraordinary, but its continuation depends on the moat holding and the AI cycle not cooling sharply.

The CUDA software ecosystem is the main defense against these risks, raising the cost for customers to switch away. But it is not impregnable, and watching whether large customers deepen or diversify their Nvidia commitments is the clearest signal of how durable the growth engine will prove.

Pros and Cons of the Growth Outlook

Nvidia’s revenue growth outlook has clear strengths and clear risks. The pros: dominant data center position, structural AI demand, a powerful CUDA software moat, the H200-to-China catalyst, strong margins, and a stable gaming base beneath the AI surge.

The cons: heavy reliance on a few large customers, rising competition and custom silicon, semiconductor cyclicality, regulatory and policy exposure, and the simple mathematical challenge of maintaining high percentage growth on an ever-larger revenue base.

The pattern is clear. The drivers of growth are powerful and largely intact, but the law of large numbers and competitive pressures mean the pace will likely moderate over time. The question is not whether growth slows, but how gracefully.

What the Growth Trajectory Means for Investors

Analysis is only useful if it informs a view, so this section translates the growth story into what to watch, how to think about the deceleration that inevitably comes, and a final assessment. None of this is investment advice — consulting a licensed advisor before acting is wise.

Key Metrics to Watch

The most useful thing an investor can do is track the inputs that drive the growth story. Quarterly data center revenue growth is the single most important figure, followed by hyperscaler capital spending guidance and any concrete updates on H200 shipments into China.

Gross margins reveal whether pricing power is holding as the business scales, and commentary on competition or customer custom-silicon efforts signals long-term risk to the growth engine.

Watching these consistently gives a data-driven read on the trajectory. They tell you whether the growth story is strengthening, holding, or beginning to cool well before the headline numbers make it obvious.

It also helps to compare guidance against actual results over several quarters. A company that consistently meets or exceeds its own forecasts builds credibility, while repeated shortfalls would be an early warning that the growth engine is losing steam.

Understanding Growth Deceleration

A crucial concept for interpreting Nvidia’s revenue growth is deceleration. As the revenue base grows enormous, maintaining the same high percentage growth becomes mathematically harder, so some slowing is natural and expected rather than a sign of failure.

The market’s reaction to deceleration matters more than the deceleration itself. A slowdown to a still-strong growth rate can spook a market priced for continued acceleration, causing volatility even when the business performs well.

The practical discipline is to distinguish healthy moderation from genuine weakness. Growth cooling from extraordinary to merely strong is very different from growth stalling, and conflating the two leads to poor decisions.

Final Assessment of Nvidia’s Growth

Weighing everything, Nvidia’s revenue growth rests on powerful, structural drivers — AI-fueled data center demand, a strong software moat, and now the H200-to-China catalyst — balanced against real risks from competition, concentration, and cyclicality.

The honest conclusion is that the growth story remains compelling but will likely moderate as the base expands and competition matures. Whether that moderation is gradual or abrupt is the key uncertainty for investors.

For your own analysis, focus on the fundamentals that drive the growth rather than the headline numbers alone. To stay grounded, following each quarter’s data center results and guidance is the smartest ongoing habit before making any decision.

See More:

- 3060 Ti vs 9060 XT

- Nvidia Shield TV Pro

- RTX 5070 vs RX 9060 XT

- RTX 3090 24GB

- Nvidia price prediction

Conclusion

Nvidia revenue growth is powered overwhelmingly by AI-driven data center demand, supported by a stable gaming base and boosted by catalysts like the H200-to-China opening. The drivers are structural and the moat is strong, but competition, customer concentration, cyclicality, and the simple math of a growing base mean the pace will likely moderate over time. For investors, the key is distinguishing healthy deceleration from real weakness and tracking the metrics that actually drive the story. Keep following Nvidia’s quarterly data center revenue and guidance so your read on its revenue growth stays current. This article is informational and not financial advice.

Write Your Review

No reviews yet. Be the first to share your experience!