Any nvidia price prediction 2030 comes with a huge caveat: forecasts this far out are educated guesses, not certainties, and published targets range from spectacular gains to steep declines. With NVIDIA already one of the world’s most valuable companies, analysts disagree sharply on whether the AI boom powering it can sustain years more growth. This guide lays out the bull, base, and bear cases behind the various 2030 predictions, the assumptions driving them, and how to think critically about any long-term forecast rather than taking a single number at face value.

Understanding NVIDIA Price Prediction 2030

Predicting a stock price five or more years out is inherently uncertain, and NVIDIA is an especially hard case given how much rides on the still-evolving AI boom. Published 2030 targets vary enormously because they depend on assumptions about growth, margins, and market conditions that no one can know in advance. Understanding why the forecasts differ so much is the key to reading any of them sensibly.

Why Forecasts Vary So Widely

Long-term price predictions rely on forecasting methods that each carry large uncertainties. Analysts use discounted cash flow models, apply valuation multiples to projected earnings, or extrapolate growth rates, and each approach is highly sensitive to its underlying assumptions.

Small changes in assumed growth or the future valuation multiple compound into vastly different 2030 outcomes. A model assuming continued hypergrowth and a high multiple produces a very different number from one assuming normalization, even with similar starting points.

This is why credible sources publish 2030 targets that differ by huge margins. The dispersion reflects genuine uncertainty about the future, not a failure of analysis, so no single prediction should be treated as authoritative. The wide spread is itself the most useful takeaway, since it signals that anyone claiming precision about a 2030 price is overstating what can genuinely be known.

Where NVIDIA Stands Now

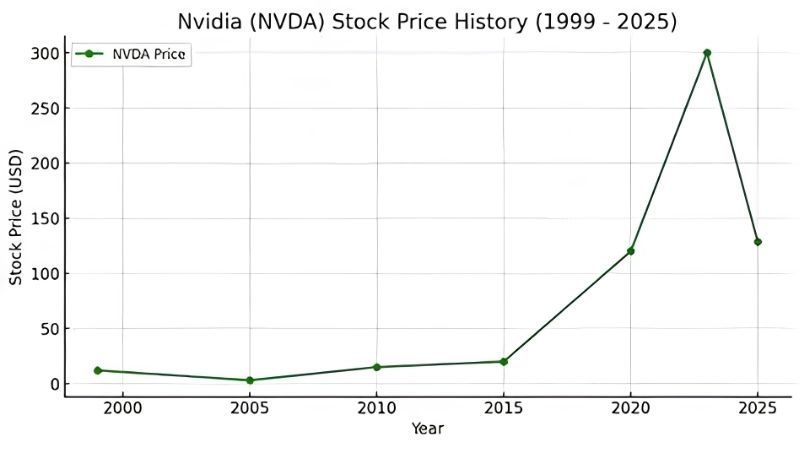

To judge any forecast, it helps to know the starting point. As of mid-2026, NVIDIA shares traded around $190 to $210 following a ten-for-one stock split, and the company had become the first to reach a market capitalization near $5 trillion.

Its fundamentals remain exceptional, with record revenue, gross margins near 75%, and roughly 90% of the AI accelerator market. Analysts are overwhelmingly bullish in the near term, with twelve-month price targets generally implying further upside. That near-term optimism, though, tells you little about where the stock lands years from now.

This is the base from which 2030 predictions extend. Any long-term target is effectively a bet on how much more a company of this scale can grow over the following years, which is where opinions diverge sharply. At this scale, even continued strong growth produces smaller percentage gains than in NVIDIA’s earlier years, a mathematical reality that tempers the most aggressive projections.

The Range of Published 2030 Targets

Published 2030 predictions span an enormous range. Toward the optimistic end, some analysts model prices around $490 in bullish scenarios, while others suggest figures in the $750 to $970 area under more aggressive AI-growth assumptions.

Base cases tend to cluster more modestly, with several analysts projecting prices in the $240 to $265 range if growth continues but at a slower pace. These reflect solid but not spectacular outcomes from current levels.

The bear cases are sobering, with some models suggesting a decline to well under $100 if the AI narrative falters. Reputable sources can sit thousands of dollars apart once these figures are translated into market caps. This spread, from steep loss to multi-fold gain, captures just how uncertain a 2030 forecast truly is. Rather than choosing one figure, it is more instructive to note the full range and the assumptions that would have to hold for each end of it to come true.

The Cases Behind the Predictions

Each prediction rests on a scenario for NVIDIA’s business. Here are the bull, base, and bear arguments that produce these widely differing numbers.

The Bull Case

The bull case rests on continued AI dominance. Supporters point to NVIDIA’s roughly 90% share of AI accelerators, its entrenched CUDA software moat, and projections that the AI infrastructure market could reach into the trillions by 2030.

In these scenarios, data center revenue keeps compounding at a high rate, potentially tripling by 2030, while margins stay above 70% thanks to limited high-end competition. Hyperscaler spending commitments, running into the hundreds of billions, underpin the demand.

If these assumptions hold, some models see NVIDIA’s market capitalization climbing well beyond $10 trillion, driving the highest price targets. The bull case is essentially a bet that the AI build-out is still in its early innings. Proponents argue that today’s spending represents the beginning of a multi-year infrastructure cycle, comparable in scale to earlier technology transitions that ran for a decade or more.

The Base Case

The base case assumes strong but moderating growth. Here NVIDIA remains the AI leader, but its expansion slows as the market matures, competitors gain some ground, and the extraordinary growth rates of recent years gradually normalize.

These scenarios still involve substantial revenue growth, just at a more sustainable pace, with the valuation multiple easing from today’s elevated levels. The result is meaningful but not dramatic upside from current prices.

Base cases represent what many analysts view as the most likely path: continued success without the AI narrative either collapsing or exceeding today’s lofty expectations. It is the middle ground between the extremes. For many analysts this scenario is the anchor, treating spectacular gains and steep losses as the tails around a more probable path of solid, decelerating growth.

The Bear Case

The bear case centers on the risks. It assumes AI spending slows or proves less durable than hoped, competition from custom chips and rivals like AMD and Huawei erodes NVIDIA’s share, and its high valuation contracts sharply.

Export restrictions add to the concern, with the China market, worth an estimated $50 billion, remaining uncertain, and any tightening removing potential revenue. In these scenarios, growth stalls and the premium investors pay today evaporates.

The most bearish models see a steep decline by 2030. While many consider this outcome unlikely given NVIDIA’s dominance, it illustrates the downside if the assumptions underpinning the bull case fail to materialize. History offers precedents of high-flying leaders whose growth normalized faster than expected, a reminder that no dominance is permanent in a fast-moving industry.

Making Sense of NVIDIA Price Prediction 2030

With the cases laid out, the goal is not to pick a number but to think clearly about the odds. This section weighs what could go right against what could go wrong, and how to use forecasts responsibly.

What Could Make the Bulls Right

The bull case gains credibility from real strengths. NVIDIA’s dominant market share, deep software moat, relentless product cadence with Blackwell and Rubin, and enormous locked-in demand from hyperscalers all support the argument for continued growth.

The scale of projected AI infrastructure spending is genuinely vast, and if NVIDIA retains most of its share, high revenue growth through 2030 is plausible. Its high margins and cash generation reinforce the case.

These are not fanciful assumptions but extensions of current trends. If the AI build-out continues at anything like its recent pace, the more optimistic 2030 targets become defensible rather than fantastical. The key uncertainty is duration, not direction, since almost everyone agrees NVIDIA will grow, and the debate is really about how long the current pace can persist.

What Could Make the Bears Right

The bear case draws on equally real risks. Growth is already showing early signs of slowing across some metrics, valuation remains elevated versus peers, and the stock is arguably priced for perfection, leaving little room for disappointment.

Competition, export policy, and the possibility of an AI spending slowdown are all genuine threats that could derail the growth story. Concentration in a few large customers adds vulnerability if their spending pulls back.

None of these guarantee a poor outcome, but they explain why cautious forecasts exist. A prudent view acknowledges that even a dominant company can disappoint if expectations are set too high. The bear case does not require NVIDIA to fail, only to fall short of the near-perfection its valuation already assumes, which is a lower bar than it might first appear.

How to Use Forecasts and a Disclaimer

The sensible way to use any 2030 prediction is as a framework for thinking, not a promise. Focus on the assumptions behind a target and whether you find them reasonable, rather than fixating on the headline number itself.

This overview is educational and firmly not financial advice. Long-term forecasts are speculative and frequently wrong, so anyone making investment decisions should do their own thorough research and consider consulting a qualified financial professional.

If your interest in NVIDIA extends to its products as well as its stock, the same technology behind these forecasts powers its consumer graphics cards. Gamers and builders can use the link to explore current NVIDIA GPUs directly. Following the products gives a grounded sense of NVIDIA’s competitive position, which is ultimately what any long-term forecast is trying to predict.

See more:

- amd driver auto-detect tool

- nvidia geforce rtx 5080 best buy

- TechPowerUp GPU-Z

- nvidia china

- nvidia etf price

Conclusion

Any nvidia price prediction 2030 spans an enormous range, from bullish targets near $490 or higher to base cases around $240 to $265 and bear scenarios well below $100, reflecting deep uncertainty about whether the AI boom can sustain years more growth. The bull case rests on continued AI dominance, the bear on competition, policy, and stretched valuation, and no one can know which will prove right. Treat every forecast as a framework built on assumptions, not a promise, and remember this is analysis, not financial advice. If you follow NVIDIA’s products too, use the link above to explore its current graphics cards.

Write Your Review

No reviews yet. Be the first to share your experience!